|

|

|

|

In this action the petitioner [Plaintiff] contended that the New York State Department of Education's [SED] denial of his application for clearance for employment as a teacher was arbitrary and capricious.

The Appellate Division, noting that "In a CPLR article 78 proceeding to review a determination of an administrative agency, the standard of judicial review is whether the determination was made in violation of lawful procedure, was affected by an error of law, or was arbitrary and capricious or an abuse of discretion", agreed with the Supreme Court's holding that SED's determination was not arbitrary and capricious, and affirmed the Supreme Court's dismissal of Plaintiff's petition challenging the SED's determination.

In the words of the Appellate Division, "An action is arbitrary and capricious when it is taken without sound basis in reason or regard to the facts. When a determination is supported by a rational basis, it must be sustained even if the reviewing court would have reached a different result".

Click HERE to access the Appellate Division's decision posted on the Internet.

In this action the Appellate Division affirmed a Supreme Court's ruling that a prior decision denying CPLR Article 78 relief bars a subsequent plenary action where, as here, the same issues were raised, fully litigated, and necessarily decided.

Further, the Appellate Division opined that even if the above claims were not barred, the complaint fails to state a cause of action as his religious discrimination claims fail to connect Plaintiff's alleged religious beliefs to the requirement for vaccination as Plaintiff's "conclusory assertions" of discrimination are "unsupported by sufficient factual allegations".

As to Plaintiff's remaining claims, the Appellate Division concluded that these were also properly dismissed for failure to state a cause of action as:

1. Plaintiff's claim for declaratory relief is moot, since the City rescinded the vaccine mandate in February 2023;

2. Plaintiff's claim for intentional infliction of emotional distress is barred as against defendant City on public policy grounds; and

3. Plaintiff's claims otherwise fails to allege extreme and outrageous conduct by the individually named defendant.

4. Plaintiff's Free Exercise claim, "[Plaintiff] has no private right of action to recover damages for violations of the New York State Constitution, since the alleged wrongs could be addressed by alternative remedies, including those pursued" here under the City HRL and State HRL"

5. Plaintiff's breach of contract claim fails for lack of standing as Plaintiff "has no individual right to enforce the collective bargaining agreement".

Click HERE to access the Appellate Division's decision posted on the Internet.

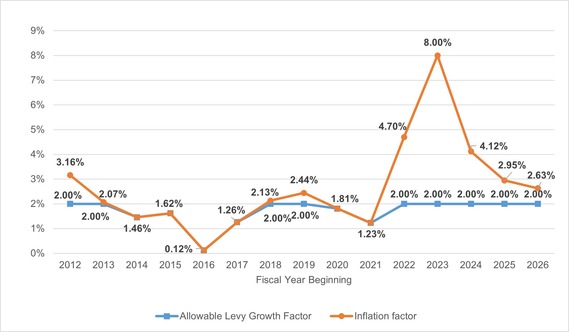

On January 14, 2026, New York State Comptroller Thomas Peter DiNapoli announced school district tax cap levy will remain at 2%.

Property tax levy growth for New York’s school districts and 10 cities will remain capped at 2% for the fifth year in a row, according to data released on January 14, 2026, by State Comptroller DiNapoli.

The tax cap, which first applied to local governments (excluding New York City) and school districts in 2012, limits annual tax levy increases to the lesser of the rate of inflation or 2% with certain exceptions. The law includes provisions that allow school districts and municipalities to override the cap. DiNapoli’s office calculated the inflation factor at 2.63% for those with a June 30, 2027, fiscal year end.

“For the fifth consecutive year, the property tax levy for school districts and 10 cities will be capped at 2%,” DiNapoli said. “School district and municipal officials must continue to find ways to deliver services efficiently as they deal with higher costs and the potential impact of federal actions.”

The 2% allowable levy growth affects the tax cap calculations for 675 school districts and 10 cities with fiscal years starting July 1, 2026, including the “Big Four” cities of Buffalo, Rochester, Syracuse and Yonkers, as well as Amsterdam, Auburn, Corning, Long Beach, Watertown, and White Plains.

Note: Allowable levy growth is expressed as a percentage.

List of allowable tax levy growth factors for all local governments

Real Property Tax Cap and Tax Cap Compliance web page